World’s largest economies in 2020: Euromonitor International’s forecast

In 2020, emerging markets will dominate the top five largest economies (China, USA, India, Japan and Russia), acording to Euromonitor International‘s analyst insight “Forecast: WORLD’S LARGEST ECONOMIES IN 2020”. The most symbolic shift will be when China overtakes the USA as the largest economy globally, say the authors of the study.

Emerging economies are driving global economic growth but advanced economies will retain a competitive advantage with higher per capita incomes and greater consumer market expenditure, while governments in developing countries face challenges in keeping up with the pace of economic growth.

Euromonitor predicts that the world’s five largest economies in 2020, measured in Purchasing Power Parity terms (PPP) will be:

1. China – 26,117 GDP in PPP: 2020 (I$ billion)

2. USA – 22,482 GDP in PPP: 2020 (I$ billion)

3. India – 9,297 GDP in PPP: 2020 (I$ billion)

4. Japan – 5,620 GDP in PPP: 2020 (I$ billion)

5. Russia – 4,410 GDP in PPP: 2020 (I$ billion).

The three biggest emerging economies will account for around 30.0% of global GDP in PPP terms in 2020 compared to 23.5% in 2012 when there were just two emerging markets amongst the five largest economies (1. USA 2. China 3. India 4. Japan 5. Germany). The most discernible shift in global power towards emerging market economies is expected to take place in 2017 when China will become the world’s largest economy.

Euromonitor International‘s forecast have used PPP as this is a method of measuring the relative purchasing power of different countries’ currencies over the same types of goods and services, thus allowing a more accurate comparison of living standards. PPP allows for exchange rates to adjust so that different price levels are eliminated. In terms of analysing the size of economies around the world, it allows for a more accurate comparison.

As emerging market economies expand, standards of living will improve, poverty declines, and real incomes generally rise, with a corresponding expansion of the global middle class. This will have tremendous implications for global consumer market development:

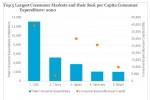

Consumer markets are seeing a similar shift towards emerging markets. In global rankings of the largest consumer markets measured by total consumer expenditure in US$ terms, China was the only emerging country in the top five in 2012, at third place (behind the USA and Japan). By 2020, Euromonitor forecasts that Brazil will join China in the five largest consumer markets in real US$ terms. Together, these two countries will account for 13.7% of global consumer spending in 2020 but this is still far behind the world’s largest consumer market, the USA, which alone will make up just under a quarter of global consumer expenditure;

The Map to Modern Luxury

THE CURATED CALENDAR

Discover the world’s most prestigious gatherings & exhibitionsHowever, in per capita terms, developing market convergence with advanced economies is a long way off with significant gaps in spending power and living standards. Switzerland and Norway will have the largest annual disposable incomes per capita in the world in US$ terms in 2020 at US$56,031 and US$50,567 respectively in real terms. In comparison, China and India, which have much larger population sizes being the most populated countries in the world, will have per capita annual disposable income of just US$5,996 and US$1,856 correspondingly. Yet, both China and India will experience amongst the fastest real growth in both consumer expenditure per capita and annual disposable income per capita in the world over 2013-2020 as their markets develop from a low base.

This contrast means that consumer goods companies and marketers will need to target advanced economies and developing countries with varying strategies and even through alteration in products or services to take into account local purchasing power capabilities. As the middle class grows in developing markets, there will be a greater propensity for discretionary spending outside of the essential categories of food and housing. Yet poverty and low incomes will remain widespread in some countries, so businesses should also consider the “bottom of the pyramid” market. In Indonesia, for example, in 2012 there were 36.7 million households with a disposable income less than US$7,500 – equivalent to almost 60% of households.

There remain many obstacles to economic growth in emerging and developing countries:Although they can benefit from young and growing populations, this is only an asset if the government or the pace of economic development and reform can keep up with job demand, otherwise it can equally end up being a source of problems and discontent, as seen most recently in the Arab Spring;

Education and skills are vital to improve human capital, attract foreign direct investment (FDI) inflows and to aid the progression from low-skilled manufacturing to higher value manufacturing, services and technological innovation;

Infrastructure deficits are a hindrance for business environments in developing countries both in terms of obstructing

the ease of the movement of goods and services but also of the labour force. Likewise, a global digital divide persists

with emerging markets lagging behind that of advanced economies in ICT and Internet penetration. Greater investment is

needed to open up access to Internet and telecommunications services, especially in rural or difficult to reach areas;

Finally income inequalities will impede full economic growth potential. Out of a ranking of 85 major economies in terms of their Gini Index (a measure of income inequality), Euromonitor figures show that the top 10 most unequal countries were all developing countries in 2012. South Africa topped the list with a score of 63.6 (the higher the number over 0, the higher the inequality, and a score of 100 indicates total inequality) while major developing countries such as China and India are seeing income inequalities rise despite their economic growth.