A deep dive into the landmark 20th edition of The Wealth Report, and why its findings matter to anyone who cares about the future of luxury, property, and private capital.

Every year, Knight Frank — one of the world’s most respected independent property consultancies — drops its Wealth Report like a stone into still water, and then we all watch the ripples. This year, though, they dropped something closer to a boulder. The 2026 edition marks the report’s 20th anniversary, and it arrives at one of the most genuinely turbulent moments in living memory: geopolitical conflict rattling energy markets, inflation refusing to lie down quietly, and a financial world recalibrating itself in real time. Against that rather stormy backdrop, the data the report serves up is — to put it plainly — extraordinary.

So let’s unpack it. Not in the language of financial analysts, but in plain terms that make sense for anyone who has ever been curious about how the seriously wealthy live, invest, and think about the future.

The Machine That Keeps Minting Millionaires

Picture a turnstile at one of the world’s busiest airports. Now imagine that every ten minutes or so, a new person worth over $30 million walks through it. That’s essentially what’s been happening across the globe for the past five years.

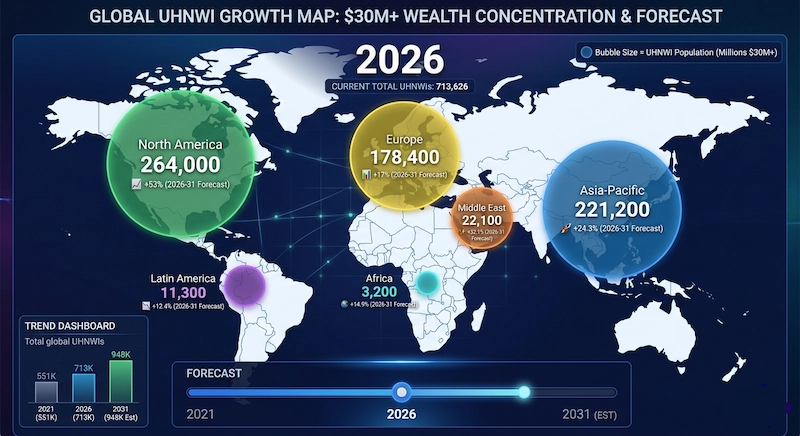

According to Knight Frank’s updated Wealth Sizing Model, the number of ultra-high-net-worth individuals — people with a net worth above $30 million, or UHNWIs in the industry shorthand — grew from 551,435 in 2021 to 713,626 in 2026. That’s 162,191 new entries into what is arguably the world’s most exclusive club, at a rate of 89 people per day, every day, for five consecutive years.

The United States is, by some distance, the engine room of this expansion. Of every ten new UHNWIs created over the period, four came from America. The US share of global ultra-wealth has climbed from 33% to 35%, and forecasts suggest it will reach 41% by 2031. This isn’t just about Silicon Valley tech founders, though that’s part of the story. It’s about the sheer scale and depth of American capital markets — the ability to generate, recycle, and compound wealth at an industrial pace that no other country currently matches.

But the US isn’t the only act worth watching. India is perhaps the most compelling subplot. Its UHNW population surged 63% between 2021 and 2026, riding on the back of booming technology, capital markets, and a generation of entrepreneurs plugged into global networks. And it’s not slowing down — a further 27% growth is forecast by 2031. Think of India as a city that spent decades building its foundations in the ground; now you’re finally starting to see the skyline rise.

Beyond India, a cluster of fast-maturing economies are sprinting up the rankings. Indonesia leads the five-year growth forecast at 82%. Saudi Arabia and Poland, both at 63%, follow close behind. Vietnam, at nearly 60%, is another name that will feature in these conversations increasingly. These aren’t flukes — they reflect genuine structural shifts in how and where value is being created in the 21st century.

Plutonomy: The Concept That Predicted Everything

In 2007, when Knight Frank first published The Wealth Report, it built the whole thing around a then-relatively obscure idea coined by a Citi analyst named Ajay Kapur: plutonomy. The basic thesis was this — in certain economies, the wealthy don’t just have more money than everyone else, they are the economy. Their spending, investing, and asset accumulation drives markets more than the behaviour of ordinary consumers does.

Twenty years on, the 2026 report revisits that original prediction with the benefit of hindsight. The verdict? Plutonomy didn’t just survive — it accelerated.

The mechanisms behind it are worth understanding, because they’re not going away. Cheap credit after the 2008 financial crisis allowed the ultra-wealthy to borrow against their assets at low interest rates while generating far higher returns on investments. Technology created new fortunes at unprecedented speed. And the globalisation of capital meant that money could flow anywhere in the world instantly, always seeking the highest return.

The political pushback is real — wealth taxes, anti-billionaire rhetoric, the rise of populism on both ends of the spectrum. David Poole, a former head of Citi Private Bank who was in the room when plutonomy was first discussed, puts it plainly: “That line can’t keep going.” The concentration of wealth creates social friction, and social friction eventually creates political friction. But here’s the thing — even as the backlash builds, the fundamental forces driving wealth concentration haven’t reversed. They’ve deepened. Plutonomy isn’t a prediction anymore. It’s just the world.

The Family Office, Reimagined

If plutonomy describes the world’s wealth concentration, family offices are how that wealth gets managed. And they are changing — fast.

There are now approximately 10,000 family offices globally, and Knight Frank’s 2026 Family Office Survey paints a picture of institutions that have grown far beyond their original purpose of simply keeping the family fortune safe. These are now professionalised investment platforms in their own right, recruiting in-house specialists, pursuing co-investment opportunities alongside private equity funds, and targeting what the industry calls “value-add” real estate — properties that need work, repositioning, or clever management to unlock their full potential.

Think of the old family office like a careful librarian: deeply knowledgeable, very organised, and focused primarily on preservation. The new family office is more like a venture fund with a very long time horizon — actively hunting for opportunities, willing to take calculated risk, and increasingly operating across multiple cities simultaneously. Some of the leaner, more tech-enabled offices are essentially running themselves like start-ups, using digital infrastructure to deploy capital across global hubs efficiently.

The geographic spread of these hubs tells its own story. London, New York, Dubai, Singapore — these aren’t just cities anymore, they’re nodes in a network that sophisticated private capital flows between. A single family might have its principal residence in one, its primary investment vehicle in another, and its children’s education rooted in a third.

The PIRI 100: The World’s Most Exclusive House Price Index

Most people are familiar with property indexes that track average house prices. Knight Frank’s Prime International Residential Index — the PIRI 100 — does something different. It tracks price movements across the world’s 100 leading luxury residential markets: the kind of places where the homes start at a price most people couldn’t pay in several lifetimes.

The 2025 data recorded a 3.2% average rise in global luxury residential prices, slightly softer than the 3.6% seen in 2024, but still outperforming broader housing markets in most economies. Behind that headline average, though, the regional variations are dramatic enough to make your head spin.

Tokyo posted a 58.5% price increase. Let that land for a moment. The Japanese capital’s luxury property market didn’t just grow — it transformed, driven by a combination of yen weakness making Japanese assets extraordinarily attractive to international buyers, and a genuine supply shortage in the premium segment. Dubai followed with a 25.1% rise, cementing its position as the Middle East’s dominant prime residential market. The wider Middle East region led globally with a 9.4% surge.

Of the 100 markets tracked, 73 saw prices increase and 24 experienced declines. The report points to Mumbai, Brisbane, and Miami as markets with meaningful further growth potential — a reminder that even in a world where prime property often feels absurdly priced, the fundamentals of supply, demand, and wealth migration can still propel values higher.

One trend the report underlines with some force: the shortage of turnkey, move-in-ready homes at the top of the market. Wealthy buyers increasingly don’t want to manage renovation projects — they want perfection, ready to go. Where that supply is short, prices are rising fast. The branded residences sector is booming partly for the same reason: buyers will pay a premium to know exactly what they’re getting.

The Structural Forces Reshaping Everything

Beneath all the headline numbers, the 2026 Wealth Report identifies a set of deeper forces that are rewiring the prime residential market from the ground up. Think of these as the tectonic plates — moving slowly, but with enormous eventual consequence.

The Map to Modern Luxury

THE CURATED CALENDAR

Discover the world’s most prestigious gatherings & exhibitionsThe most visible of these right now is tax and political risk. Wealth taxes, stamp duties, non-dom rule changes, and increasingly hostile political rhetoric toward the very wealthy are prompting a wave of mobility unlike anything seen before. The report describes a “dip-in, dip-out” lifestyle — UHNWIs maintaining strategic footholds across multiple jurisdictions, not necessarily abandoning any single city entirely, but no longer anchoring their lives and assets to one place. Tax haven versus traditional wealth hub is becoming a less binary choice; it’s more about assembling a personalised portfolio of residencies.

The second force is the chronic scarcity of quality supply. In market after market, there simply aren’t enough exceptional, ready-to-live-in homes at the top end. This is driving prices, accelerating the branded residence trend, and rewarding developers who can deliver without compromise.

Third, and perhaps most intriguing, is the AI-and-tech overlay on real estate itself. The report examines how artificial intelligence might finally unlock blockchain’s dormant potential in property transactions — making conveyancing faster, more transparent, and less prone to the sort of administrative friction that plagues even the most sophisticated markets today. Satellite infrastructure, meanwhile, is beginning to actively protect real estate assets from climate and environmental risks. The future of property is becoming genuinely technological.

Commercial Real Estate Finds Its Footing — and Diversifies

Commercial real estate has had a rough few years. Rising interest rates, the post-pandemic reinvention of office space, and general investor nervousness created a prolonged period of uncertainty. The 2026 Wealth Report signals something of a turning point.

Around $144 billion of institutional capital is preparing to re-enter the global commercial real estate market in 2026. But the more interesting story is what’s been happening in the meantime — because private capital hasn’t been waiting around. HNWIs and family offices have been the largest buyers of global commercial real estate for five consecutive years running, deploying $464 billion in 2025 alone, compared to $347 billion from institutional investors.

In Europe, large-scale office transactions are returning, with private investors putting $18.9 billion into European offices over the past year. In Asia-Pacific, cross-border HNWI investment has climbed back to its highest level since 2019. Chinese mainland capital accounts for 46% of buying interest in the region.

The diversification story is equally compelling. Data centres — the physical infrastructure that powers the AI boom — are emerging as one of the hottest investment categories in commercial real estate. These are energy-hungry, mission-critical assets that are increasingly being treated as infrastructure investments, not just buildings. Energy demand as an investment theme runs through the whole report: the electrification of the global economy is happening faster than physical infrastructure can keep up, and the gap between the two is a genuine investment opportunity.

Then there’s vineyards — perhaps the most surprising entry in the diversification conversation. Climate change is redrawing the global wine production map, with some traditional wine regions under pressure and new areas becoming viable. For investors who understand both agriculture and luxury consumer tastes, this is a niche with genuine long-term structural tailwinds.

Luxury Finds Its Balance — After the Correction

Luxury as an asset class has been through a period of adjustment. Knight Frank’s Luxury Investment Index — which tracks everything from fine art and classic cars to rare whisky and coloured diamonds — recorded a marginal -0.4% decline in 2025. That sounds modest, and the report frames it as exactly that: a stabilisation, not a collapse, after two years of broader correction across several collectible categories.

Impressionist art and watches posted solid gains. The wider market is characterised right now by buyers who are highly disciplined — not afraid to spend, but unwilling to pay above fair value. The frothy, anything-goes enthusiasm that sometimes characterises luxury investment markets has given way to something more considered.

What’s new and genuinely interesting is where the next wave of demand is coming from. Vintage haute couture is gaining traction as an investable category. Rare fossils — yes, you read that correctly — are attracting serious collector interest. And fractional ownership platforms are democratising access to luxury collectibles in ways that simply weren’t possible five years ago, opening the market to a younger, passionate demographic that might not have the capital to buy a museum-quality piece outright but can own a meaningful share of one.

The Transformation Economy: Luxury Grows Up

This is, to my mind, the most intellectually rich theme in the entire 2026 report — and the one with the broadest cultural resonance.

The report traces a shift in what the world’s wealthiest consumers actually want. For a long time, luxury was fundamentally about accumulation: the right house, the right car, the right watch, the right address. Status was displayed through objects and square footage. That model isn’t dead, but it’s no longer sufficient — particularly for younger wealthy consumers who have grown up in a world of abundance and are looking for something that accumulation can’t quite deliver.

Enter what the report calls the “transformation economy.” The idea is this: the most meaningful luxury experiences aren’t the ones that let you show the world what you have, but the ones that change who you are. Wellness retreats that genuinely transform your health and mental state. Learning experiences that give you mastery of something you care about. Communities — private members’ clubs, curated networks — that offer a genuine sense of belonging rather than just exclusivity.

The report puts it elegantly: “Luxury isn’t just about what you own — it’s about who you’re becoming.”

Brands that understand this shift are repositioning themselves accordingly. Property developers are building communities around purpose — not just amenities checklists. Private members’ clubs are rethinking their value proposition from access to transformation. The wellness economy, the experience economy, the purpose economy — these aren’t separate trends. They’re all expressions of the same underlying shift in what wealthy consumers are looking for.

It’s worth noting that this isn’t purely altruistic. The transformation economy is commercially powerful precisely because experiences are harder to commoditise than objects. You can find a cheaper version of almost any luxury good. But a truly transformative experience — one that involves genuine skill, genuine community, genuine personal growth — is difficult to replicate at scale. That’s where the real margin is, and that’s where the smartest brands and developers are heading.

The Big Picture

Step back from the individual themes and a coherent picture emerges. The world is creating wealth faster than almost anyone predicted, even in the face of genuine geopolitical disruption. That wealth is concentrating — at the top end of societies, and increasingly in the hands of private capital rather than institutions. It’s becoming more mobile, more sophisticated in how it’s managed, and more discerning in what it wants to buy.

Prime property remains a central store of value for this capital, but it’s no longer a simple story of “buy the best postcode and wait.” The locations that win are the ones that offer genuine quality of life, political stability, supply scarcity, and — increasingly — some form of meaningful experience or community. The ones that lose are the ones that assumed their historical prestige would carry them indefinitely.

And luxury itself is in the middle of a quiet but profound redefinition. The question “what does a wealthy person want?” has a different answer today than it did twenty years ago. It’s less about the trophy, and more about the transformation.

Twenty years into tracking these markets, Knight Frank’s report feels less like a snapshot and more like an ongoing conversation about what it means to create, preserve, and meaningfully deploy private wealth in a world that never stops changing. The 2026 edition makes clear: the pace of that change is only accelerating.